Iris SooJin Park

A little about me

I am currently on the 2026–2027 academic job market.

I am a PhD candidate in the Department of Risk and Insurance at the University of Wisconsin-Madison's Wisconsin School of Business, with an expected graduation in Spring 2027.

My research studies how households make insurance and financial decisions under risk, with a focus on health and life insurance, behavioral responses to insurance design, and information frictions.

Before joining the risk and insurance department, I earned undergraduate degrees in economics and mathematics from the University of Wisconsin-Madison in May 2021, graduating with distinction.

Here is a link to my CV.

Research

Working Papers

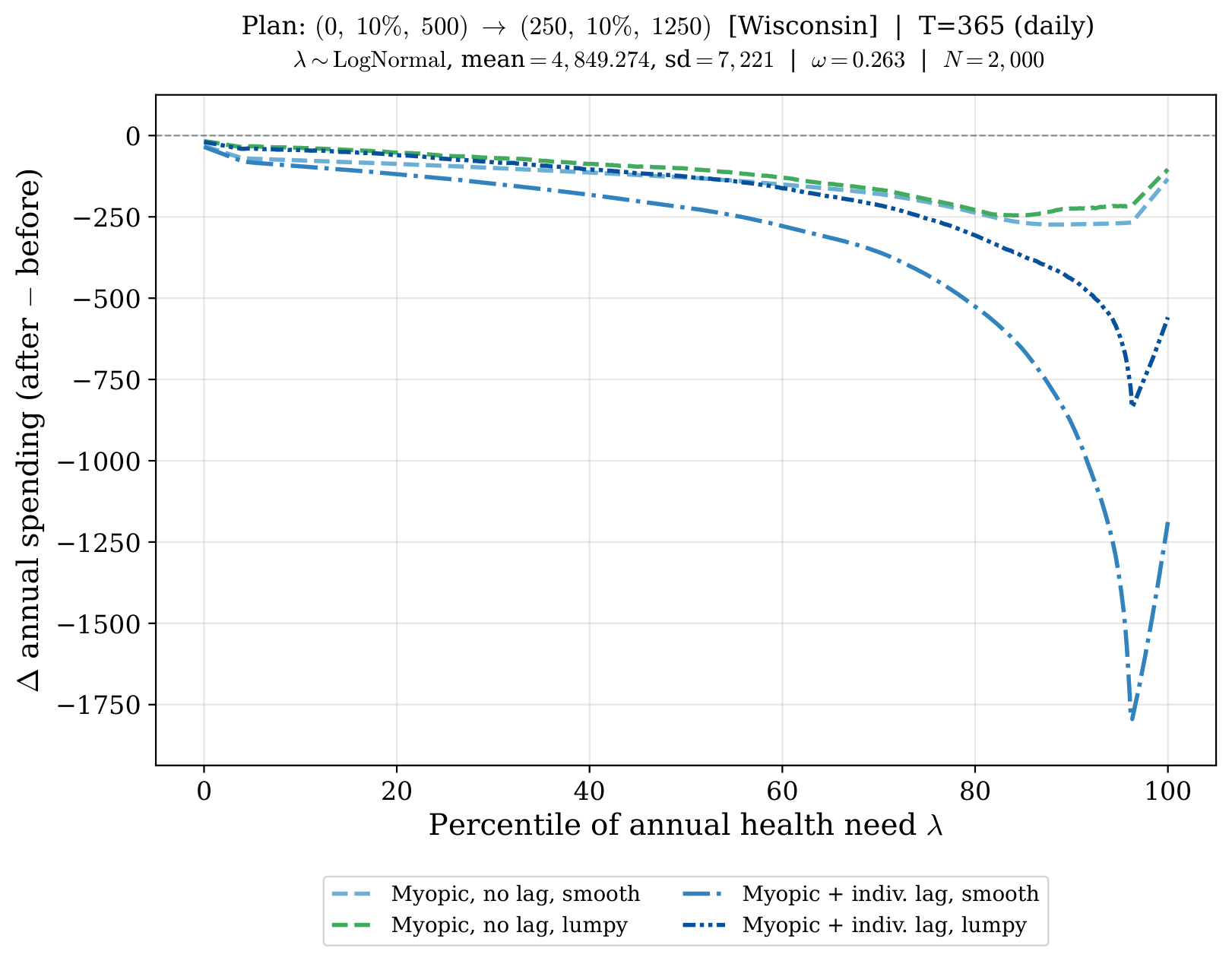

Myopia, Price Perception, and Moral Hazard in Health Insurance

Job Market Paper

Draft available soon.

I show that household myopia and price perception rationalize puzzles in health care demand. Benchmark models of health care demand assume forward-looking households that anticipate how current spending lowers future prices under health insurance with nonlinear cost-sharing. I study how employees reacted to the introduction of modest cost-sharing in a health plan that previously had zero deductibles and find evidence inconsistent with the model: aggregate spending responses are modest but increase steeply with health risk. A structurally estimated forward-looking model incorrectly predicts little response among the high-risk households who should anticipate reaching the out-of-pocket maximum. I show that this mismatch is explained by myopia and price-perception frictions. Prior work has highlighted that myopic households may respond to the spot price of care. I introduce new evidence using administrative billing data and a survey experiment that households learn about spot price adjustments slowly and often perceive spot prices imperfectly. High-risk enrollees face longer billing delays and are more likely to have claims that create a gap between average and marginal prices, generating a steep risk gradient in perceived prices. A behavioral model of moral hazard incorporating these frictions rationalizes the aggregate response and risk gradient. The results suggest that models of health care demand should account for perceived prices, not only contract incentives.

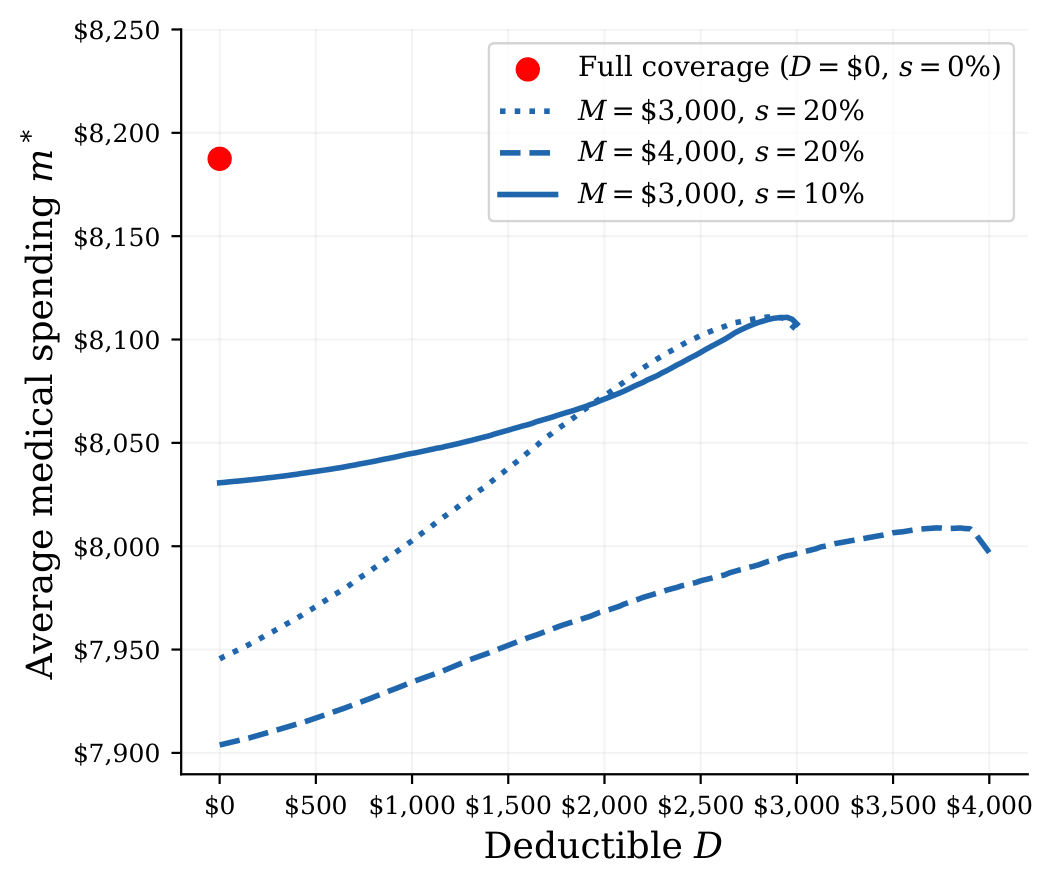

The Generosity Paradox: When Less Generous Insurance Raises Spending

Status: Under review.

This paper shows that standard models of moral hazard predict a generosity paradox: less generous insurance can increase rather than decrease medical spending. Higher cost sharing makes it easier to reach the out-of-pocket maximum, where the marginal price is zero. Forward-looking consumers near that threshold therefore optimally increase their spending to reach the maximum. Using existing empirical estimates of the health need distribution and moral hazard responsiveness, I find that in many realistic scenarios, decreases in generosity lead to aggregate increases in spending and welfare losses. I discuss the practical implications of this for plan designers.

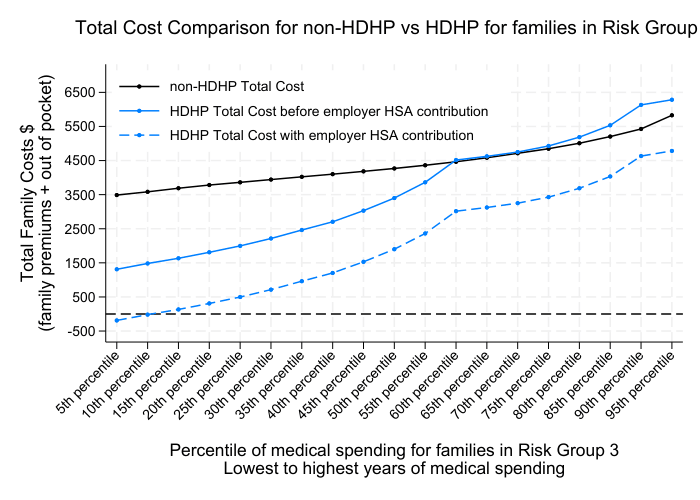

The Impact of Decision Aids on Health Insurance Selection

with Justin Sydnor and Anya Samek

🏆 The Rising Financial Literacy Scholar Award, 2026 Stanford Financial Education Symposium

Suboptimal health insurance choices impose substantial welfare costs on households, with enrollment patterns frequently violating financial dominance despite stakes exceeding thousands of dollars annually. We use a randomized field experiment with public university employees during open enrollment to evaluate whether decision aids that clarify these financial consequences affect enrollment patterns. The setting features a financially dominant high-deductible plan that saves money for all workers regardless of health spending, with typical savings around $2,000 annually, and a requirement to make an active choice confirming plan selection. We find that decision aids improve cost recognition by 22 percentage points. Yet they increase intended enrollment in the high-deductible plan by 6 percentage points and actual enrollment by only 2 percentage points, revealing substantial attenuation from understanding to behavior. Survey responses reveal that concerns about managing a health savings account, aversion to out-of-pocket costs, and reluctance to change from familiar plans limit the translation into enrollment. Treatment effects are largest among workers with limited prior plan engagement and vary substantially by liquidity constraints.

To Smooth or Not to Smooth: Consumption Responses to Life Insurance Payouts

with Tyler Welch

There is a sizable academic literature studying the demand for life insurance products. Little is known, however, about how surviving spouses utilize life insurance payouts. We study individuals 50 and older and ask how they adjust their savings, spending, and bequest behavior after life insurance payouts are received. We show that, compared to widow(er)s not receiving payouts, widow(er)s receiving life insurance payouts do not experience shocks to consumption. We also show substantial heterogeneity in other household finance responses to payouts along the wealth distribution. The wealthiest survivors tend to save their payouts, spend down slowly, and experience little change in their bequest plans. The least wealthy, on the other hand, experience enhanced bequest motives for a short period before quickly spending their payouts. In the long run, these individuals even end up more likely to be receiving government support than widow(er)s without life insurance payouts.